By: Peter Cavelti

We’re in week seven of the Russian invasion of Ukraine and much has been said and written on the subject.

The implications for the global political balance and the world economy are considerable. Some regions, like Europe, are affected in a very direct way, but the reverberations will be felt everywhere.

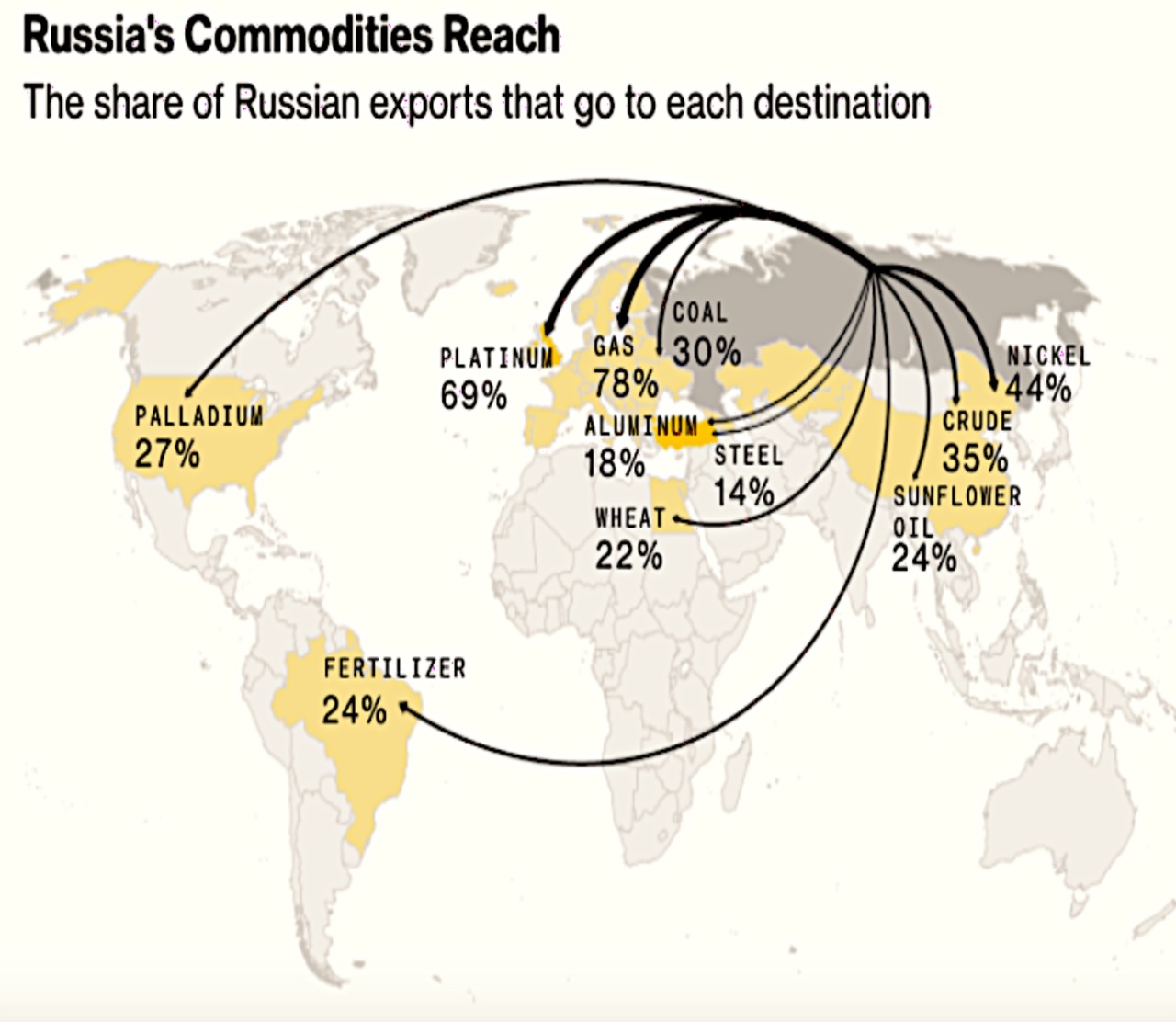

Before we turn to our investment policy review, I’d like to say a few things about one particular aspect of the conflict—that of sanctions. Why elaborate on the sanctions regime? Because it brings with it a plethora of completely underappreciated, unintended consequences. Let me elaborate. The sanctions model, long a preferred U.S. instrument, has now been pushed to its limits. The chart below shows the sheer scope of what has been unleashed. President Biden has stated that the aim of U.S. sanctions is to estrange the Russian people from their leadership. Is that what will happen? Perhaps, but it’s also worth exploring the unintended consequences.

Let’s first consider the broad context of U.S. sanctions regimes in recent years. For some time now, governments and corporations in the West and elsewhere have been alienated by America’s indiscriminate dishing out of sanctions—sometimes in the name of national security, sometimes to gain trade advantages, but almost invariably without substantive merit. One of the most offensive examples of sanctions abuse was the 2020 decision to target the Chief Prosecutor and several members of the International Criminal Court after they decided to probe U.S. war crimes committed in Afghanistan. Another was the imposition of tariffs on Canadian steel and aluminum exports in the interest of national security—imagine Canada, America’s friendly neighbour and one of its most trusted allies, being a threat to U.S. security. In short, under different circumstances than those in play in Ukraine at the moment, the duplicity of U.S. sanctions would have evoked frustration and even anger, both among America’s friends and foes. Remember that just a few months ago, Germany’s government fought to have the Nordstream 2 pipeline completed and the sanctions the U.S. imposed on it removed. French President Macron, meanwhile, kept emphasizing that the West should use a more inclusivist approach with Moscow. But the invasion of Ukraine changed all that. Russia’s brazenness was deeply resented and, for a few days, Europe felt united in its sense of betrayal. Siding with America seemed the best option available.

Yet, after an initial enthusiastic endorsement of the American sanctions platform, cracks appeared. France, which draws much of its energy from nuclear reactors, could afford to maintain a hard line. Germany’s situation is entirely different. Merkel’s government imprudently shuttered most nuclear energy plants, so that the country heavily relies on Russian natural gas.

Last year, Russia supplied more than half of Germany’s gas imports. Worse, Germany along with most other European nations is also dependent on a range of other Russian key commodities. Staying the course of the sanctions will virtually guarantee that the pan-European economy will suffer gravely.

There are other, equally negative consequences to the U.S. sanctions project, which in most cases will hurt America itself. Among the most apparent outcomes are that more Russian oil and commodities will go to China and that the demise of key elements of the postwar U.S.-led global order will be hastened. The gradual replacement of the U.S. dollar as the world’s reserve currency has been underway for a couple of years; sanctioning Moscow’s access to the Swift payment system quickly led to China allowing Russia to use its UnionPay banking system.

Much more is yet to come as non-Western nations settle their trade-in non-dollar currencies. As I mentioned in our last issue, there are several highly unstable, but strategically important countries that will be seriously impacted by shortages and rising prices. As I’m writing, Sri Lankans are rioting, while people in several of Asia’s and Africa’s urban centres are taking to the streets. The problem for the U.S.: with the Ukraine war triggering further military deployments in Europe, America’s ability to react to crises elsewhere is diminished.

Another less talked about consequence of the sanctions will play out in a series of developing economies currently close to the United States. I’m thinking of nations like Brazil or Argentina, Egypt or Nigeria, India or the Philippines. They’re all strategically important and they’re all plagued by massive corruption. There is no doubt that those in key political or corporate positions will have taken note of what just happened to Russia’s elite. The only way for them to avoid a similar fate if they deviate from America’s directives will be to distance themselves, or at least hedge their current exposure by developing alternatives to U.S. trade, payment systems and currency linkages.

In short, while there can be no doubt that the sanctions in place are punitive to Russia, they also have the effect of accelerating the transition from a unipolar world to a multi-polar one. Age of Consequences In many ways, the unintended consequences of past ill-conceived actions are manifesting all around us. Consider how the age of consumerism has led to excessive debt burdens; imprudent central bank practices and out-of-control government spending have triggered serious price inflation; trade protectionism and sanctions have made us more vulnerable to shortages; corporate spending on share buybacks instead of productive investment has inflated stock prices and undermined the economy; financial misallocation has diminished the quality of education and health care; agriculture is woefully addicted to excessive application of fertilizers, which are now harder to get. I could go on and on. The Covid pandemic and now the war in Ukraine have exposed these shortcomings for all to see. They’re also providing a convenient excuse for the ranks of politicians and corporate agitators who’ve got us into these predicaments.

Unfortunately, analyzing what went wrong at which time and considering whose fault it is won’t help us in protecting ourselves financially or in any other way. What will be of help is taking responsibility for our individual and communal destiny. By necessity, that involves letting go of our biases and giving up on narratives that confirm them. Self-styled experts and their detailed forecasts of what exactly will happen may make us feel good, but the chances that their projections prove right are ridiculously small. The bottom line is that when everything moves on an unsustainable platform, the possibilities of what lies ahead are endless. As I’ve said many times before, that does not mean that we can’t have an investment strategy. On the contrary, a disciplined approach is imperative, but it needs to allow for various outcomes and, as the situation evolves, it has to be constantly revised.

Investment Strategy During the past eighteen months, we’ve consistently dismissed the notion that inflation was a temporary phenomenon. As a result, our equity portfolio stressed exposure to natural resources and we held a significant holding in physical gold. This strategy benefited us.

Given the run-up in fossil fuel prices, the worsening shortages in food and fertilizer supplies, rising housing costs and building wage pressures, we see no reason to change our inflation-centric posture, at least for the time being. Yet, while we remain positive on the materials front, we’re getting concerned about financial markets in general.

We’ve avoided bonds for some time and instead mostly focused on top-quality equities capable of generating robust cash flow and, ideally, paying attractive dividends. Going forward, we wonder how much longer the economy and broad stock market can weather the combination of soaring commodity prices and rising short-term interest rates. If equities correct sharply, even the conservative selections we currently favour will experience a setback. As a result, we’re selectively trimming our holdings and will initiate further cutbacks on any material weakness. As it happens, the proceeds of any cutbacks end up in cash—a notoriously questionable asset in inflationary times. Even so, the risk of loss on cash positions can be mitigated by currency selection. We believe that the Euro and the Yen will continue to weaken, that the U.S. dollar will be relatively stable (despite being challenged as the world’s reserve currency) and that commodity currencies like the Canadian and Australian dollars will gain.

At least for the time being, we will follow this strategy.